Viking Therapeutics

The obesity biotech that now has to prove it can become a company

Viking Therapeutics $VKTX has spent years being discussed as a takeover candidate. That may eventually happen, but it is not a sensible investment thesis on its own.

At roughly $39 a share, Viking is valued at around $4.5 billion. After subtracting its $603 million cash and investment balance, the market is assigning approximately $3.9 billion to its pipeline and corporate infrastructure. This is no longer an overlooked biotech trading around cash. Investors are already paying a meaningful amount for clinical success.

The reason is VK2735.

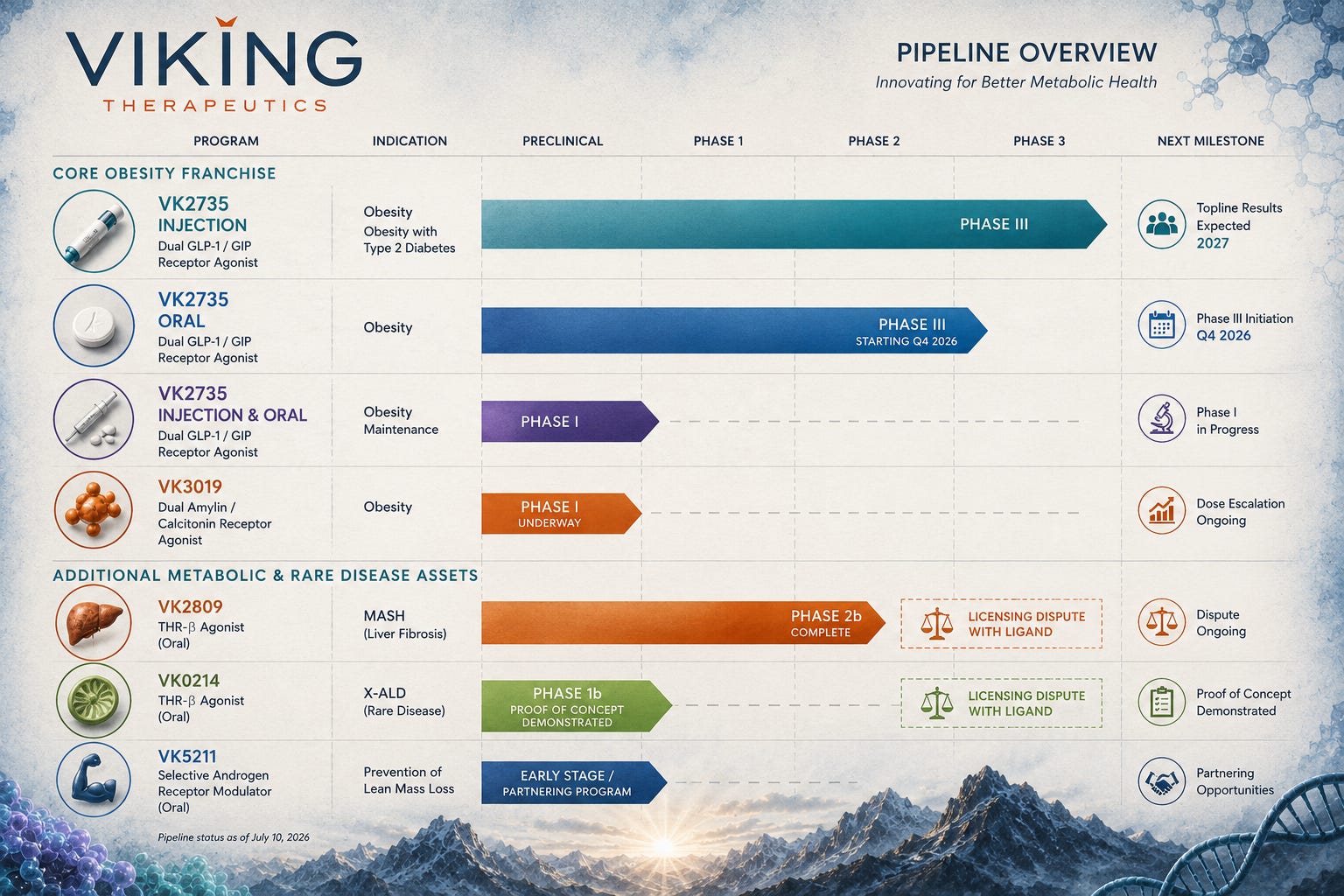

Viking has developed a dual GLP-1 and GIP receptor agonist, targeting the same two receptors as Lilly’s tirzepatide. What makes Viking particularly interesting is that it is developing VK2735 as both a weekly injection and a daily tablet. It may therefore be able to offer patients different formulations without having to build two unrelated drugs.

That is the attraction. The difficulty is proving that the results seen in relatively short Phase II trials will hold up across thousands of patients receiving the drug for more than a year.

The injection is the real investment case

In Viking’s 13-week Phase II VENTURE study, weekly injectable VK2735 produced average weight loss of as much as 14.7% from baseline and up to 13.1% after adjusting for placebo. Weight loss had not reached an obvious plateau when the study ended.

At the highest dose, as many as 88% of participants lost at least 10% of their body weight, compared with 4% receiving placebo. Those are exceptionally strong results for a study lasting only three months.

The tolerability also looked relatively manageable. Around 13% of patients receiving VK2735 discontinued treatment, compared with 14% in the placebo group. Nausea was reported by 43% of treated patients and vomiting by 18%, with one serious adverse event involving dehydration considered related to treatment.

It is important not to compare percentages mechanically across different obesity trials. Patient populations, starting weights, dose escalation and study length can all distort comparisons. Nevertheless, the Phase II injection data were strong enough to justify moving directly into a large Phase III programme.

VANQUISH-1 has enrolled approximately 4,500 adults with obesity or who are overweight with at least one related condition. Patients are receiving one of three maintenance doses—7.5 mg, 12.5 mg or 17.5 mg—or placebo for 78 weeks, followed by an extension period.

VANQUISH-2 has enrolled approximately 1,000 patients with obesity or overweight and type 2 diabetes. It uses the same three doses and also runs for 78 weeks. Enrollment in both trials is now complete, with the principal Phase III readouts expected in 2027.

This is where the real company-making risk sits. A 13-week Phase II trial can show that a drug is active. A 78-week Phase III programme reveals whether people can remain on it, whether efficacy continues to build and whether uncommon safety issues begin to appear.

Should VANQUISH reproduce the Phase II profile, Viking would possess one of the most valuable unpartnered metabolic assets in biotechnology. Should discontinuations rise materially or weight loss flatten earlier than expected, the present valuation would become much harder to defend.

The oral tablet works, but it is not yet clean

The oral version of VK2735 has produced impressive weight-loss figures of its own.

In the 280-patient VENTURE-Oral Phase II study, the highest 120 mg dose produced average weight loss of 12.2% after 13 weeks, equivalent to approximately 26.6 pounds. The placebo-adjusted reduction was 10.9%. As many as 97% of patients achieved at least 5% weight loss, while up to 80% lost at least 10%. Once again, the weight-loss curve had not clearly plateaued.

That is the positive part of the oral story.

The problem was tolerability. Across the active treatment groups, 20% of participants discontinued because of adverse events, compared with 13% on placebo. Total discontinuations reached 28% on VK2735 versus 18% on placebo.

At the highest 120 mg dose, 38% discontinued treatment early. Nausea affected 60% of patients in that group and vomiting 35%, although the company said gastrointestinal events were generally concentrated around the beginning of treatment and declined over time.

This does not make the oral drug a failure. It means the dosing schedule requires work.

Viking can use a lower starting dose, slower escalation and possibly a lower maintenance dose in Phase III. An exploratory part of the Phase II study also suggested that patients who were stepped down from 90 mg to 30 mg maintained most of their weight loss, finishing 9.2% below baseline. That may prove useful when designing a longer and more tolerable regimen.

Following its end-of-Phase-II meeting with the FDA, Viking expects to begin an oral Phase III programme in the fourth quarter of 2026. The design will matter almost as much as the eventual result. A carefully titrated tablet producing slightly less weight loss with materially fewer discontinuations could be commercially more useful than chasing the highest possible dose.

For now, I would treat the injection as the core asset and the oral formulation as meaningful upside. An investment case that requires the 120 mg oral dose to succeed exactly as tested is unnecessarily fragile.

The most interesting 2026 catalyst may not be Phase III

Viking now treats maintenance as a distinct part of its obesity franchise rather than simply an extension of the pivotal programme. On the company’s official pipeline, the maintenance study sits alongside the injectable and oral obesity programmes as its own development programme.

The Phase I study is enrolling approximately 180 adults. Participants first receive 19 weeks of weekly injectable VK2735 before being randomised to different maintenance strategies, including weekly, every-other-week and monthly injections, as well as weekly and daily oral dosing. Results are expected during the third quarter of 2026.

This isn’t designed to prove efficacy in the same way as VANQUISH. Instead, it explores how patients might realistically stay on treatment after achieving meaningful weight loss. If Viking can demonstrate that patients maintain most of their weight while reducing injection frequency or switching to oral therapy, it would create a much broader commercial franchise rather than simply another weekly obesity drug.

Obesity treatment is increasingly likely to become a long-term market rather than a short course of therapy. A considerable number of patients regain weight after stopping treatment. Cost, injection fatigue, gastrointestinal side effects and the inconvenience of weekly dosing may therefore become as important as the maximum amount of weight lost.

Suppose a patient could use the weekly injection for the initial weight-loss phase and then maintain most of that loss with a monthly injection or weekly tablet. Viking would have something more differentiated than another GLP-1 competing solely on headline efficacy.

The study is small and exploratory, so it cannot prove a commercial maintenance strategy on its own. But a convincing result would give Viking a more coherent franchise: intensive treatment, oral treatment and lower-frequency maintenance, all built around the same molecule.

Viking is also building a second obesity programme

In June, Viking began a first-in-human study of VK3019, an internally developed dual amylin and calcitonin receptor agonist.

The initial Phase I trial is testing single subcutaneous doses in adults with a BMI of at least 30, primarily examining safety, tolerability and pharmacokinetics. Viking has reported encouraging weight reduction in preclinical animal studies, but VK3019 remains far too early to assign substantial value to it.

The strategic logic is still clear. Amylin-based drugs may eventually be used alone, in combination with incretin therapies or as maintenance treatments. Novo Nordisk, Lilly, Roche and others are all investigating mechanisms beyond conventional GLP-1 drugs.

VK3019 gives Viking another way to participate if the obesity market begins moving towards combinations. It also makes the company less dependent on a single scientific mechanism, although it will be several years before investors know whether the molecule is genuinely differentiated.

VK2809 should have been a valuable second asset

Outside obesity, Viking has generated strong data with VK2809, an oral thyroid hormone receptor beta agonist being developed for metabolic dysfunction-associated steatohepatitis, or MASH.

In the Phase IIb VOYAGE study, up to 75% of patients achieved MASH resolution without worsening of fibrosis, compared with 29% receiving placebo. As many as 57% achieved at least a one-stage improvement in fibrosis without worsening of MASH, compared with 34% on placebo. The treatment was also reported to have an adverse-event profile broadly similar to placebo.

Those results would ordinarily make VK2809 an important part of Viking’s valuation.

There is now a serious complication.

In April 2026, Ligand Pharmaceuticals purported to terminate the licence covering Viking’s thyroid hormone receptor beta (TRβ) programme, including VK2809 and VK0214. Viking disputes the validity of the termination and says it intends to defend its contractual rights.

Until that dispute is resolved, I would assign limited value to VK2809. Losing the licence would remove what appeared to be Viking’s most advanced non-obesity asset. Even a negotiated settlement could introduce new payments, royalties or development obligations.

The dispute does not appear to threaten VK2735. Viking reports owning the intellectual property surrounding its GLP-1/GIP programme, including US and international patents and pending applications. The Ligand issue is therefore an overhang on the secondary pipeline rather than an existential threat to the central obesity programme.

Viking also retains two smaller programmes that receive far less investor attention. VK0214 is an oral thyroid hormone receptor beta (TRβ) agonist for X-linked adrenoleukodystrophy (X-ALD), where a Phase Ib study demonstrated proof of concept through reductions in very-long-chain fatty acids. However, like VK2809, it forms part of the ongoing licensing dispute with Ligand Pharmaceuticals.

VK5211 is a selective androgen receptor modulator (SARM) designed to preserve lean muscle mass. It remains part of Viking’s pipeline but appears to be a lower strategic priority than the obesity franchise. Unlike VK2809 and VK0214, VK5211 is not affected by the Ligand dispute.

Neither programme currently drives the investment case.

The balance sheet is strong, but not as strong as it first appears

At approximately $39 a share, Viking Therapeutics is valued at around $4.5 billion. The company held $603 million in cash, cash equivalents and short-term investments at 31 March 2026, leaving a rough cash-adjusted valuation of approximately $3.9 billion for the pipeline and business.

Viking spent $150.2 million on research and development during the first quarter and used $114 million of operating cash. That quarterly outflow should not be treated as a fixed burn rate, because the timing of clinical invoices, manufacturing commitments and prepayments can produce considerable variation. It nevertheless demonstrates how expensive the VANQUISH programme has become.

Management believes its existing resources will fund operations through at least 30 June 2027. Viking also states plainly that it will require additional capital to complete its ongoing and planned trials. The company had $63.7 million of capacity remaining under its existing at-the-market programme at the end of March, but a larger financing, partnership or other strategic transaction may eventually be required.

Dilution is therefore not a remote risk. It is part of the likely financing path.

That does not necessarily make the shares unattractive. Raising several hundred million dollars would be manageable if Phase III data substantially increased the value of VK2735. The danger is being forced to raise during a weak biotech market or after an inconclusive clinical update.

Viking is preparing as though it may commercialise the drug itself

Viking has signed broad manufacturing agreements with CordenPharma covering both injectable and oral VK2735.

The planned capacity includes multiple metric tonnes of active pharmaceutical ingredient each year, up to 100 million autoinjectors, another 100 million vial or syringe products and more than one billion oral tablets annually. The agreements can also be expanded.

This is a significant commitment for a company with no commercial products. It suggests Viking is not simply conducting enough development work to attract a buyer. Management is attempting to preserve the option of launching VK2735 itself or entering a partnership from a stronger negotiating position.

The agreements also create financial and execution risk. Viking is making prepayments against future manufacturing orders, while remaining dependent on third parties to produce commercial-scale quantities that meet regulatory standards.

Manufacturing obesity medicines is not a minor detail. Novo Nordisk and Lilly have spent billions expanding capacity, and shortages have repeatedly constrained the market. A successful drug that cannot be produced reliably is not a successful commercial product.

Competition will be brutal

Viking is entering a market already dominated by two of the largest pharmaceutical companies in the world.

Lilly and Novo Nordisk have approved drugs, established prescriber relationships, global reimbursement teams and enormous manufacturing programmes. Behind them is an expanding group that includes Amgen, Roche, Pfizer and several smaller biotechnology companies developing oral drugs, longer-acting injections, amylin combinations and muscle-preserving treatments.

The eventual obesity market may exceed $100 billion in annual sales, which means Viking would not need to beat every competitor to create substantial value. Even a small share could support several billion dollars of revenue. But a large market does not automatically produce attractive economics for every participant. Competition could force discounts, higher rebate payments and expensive head-to-head studies.

VK2735 therefore needs to establish a reason to exist beyond being another effective weight-loss drug.

That reason could be unusually rapid initial weight loss. It could be an effective oral formulation. It could be monthly maintenance. It could be a favourable tolerability profile at lower doses. At present, Viking has several possible points of differentiation, but none has yet been proven in a registrational trial.

What is the market assuming?

At the current price, Viking’s valuation is neither obviously excessive nor obviously cheap.

The market is assigning substantial value to VK2735, but nowhere near the value of a fully approved, commercially validated obesity franchise. That leaves room for the shares to rise considerably if Phase III succeeds, while also leaving plenty to lose if the programme disappoints.

Analysts remain overwhelmingly optimistic. The current average 12-month target compiled by TipRanks is approximately $92.91, with targets ranging from $70 to $125. That implies around 139% upside. H.C. Wainwright has maintained a $102 target, while Truist has used $83.

These targets are useful as a measure of sentiment, not as evidence of intrinsic value. Most assume successful development of VK2735 and some probability of a partnership or acquisition. They offer little protection if the pivotal programme fails.

In a bullish outcome, injectable VK2735 reproduces its Phase II efficacy, discontinuations remain manageable, the maintenance study demonstrates flexible dosing and the oral programme advances with an improved titration schedule. Viking could then become a serious independent obesity company or one of the most obvious large-scale acquisition targets in biotechnology.

In a more moderate outcome, the injection succeeds but proves broadly similar to other late-stage drugs, the oral formulation remains constrained by gastrointestinal side effects and Viking raises additional capital to fund commercial preparation. That could still support a valuable company, although perhaps not the spectacular outcome implied by the highest analyst targets.

In the bearish outcome, Phase III weight loss regresses towards the middle of the class, discontinuations increase over 78 weeks and Viking needs to raise money before confidence in the programme has recovered. The Ligand dispute could simultaneously remove the MASH programme from the valuation.

The conclusion

Viking is one of the more credible independent obesity developers, but the stock should not be treated as a cheap buyout ticket.

The injectable version of VK2735 is the reason to own it. Its Phase II performance was strong enough to justify the excitement, and enrollment of two large Phase III trials has been completed impressively quickly.

The oral version is promising but needs a better tolerability profile. VK3019 is interesting but extremely early. VK2809 has good clinical data but is trapped inside a licensing dispute. The company has enough cash to continue operating, although probably not enough to reach the complete Phase III outcome and build a commercial organisation without further financing.

The Q3 maintenance data could be the most important near-term signal. Monthly injections or weekly oral maintenance would give Viking something more strategically interesting than another once-weekly incretin.

At approximately $4.5 billion, investors are paying for a genuine probability of success, but not yet for category leadership.

Viking does not need to replace Lilly or Novo Nordisk. It needs to prove that VK2735 can occupy a durable place beside them.

That remains possible.

It is simply much harder than producing 13 weeks of excellent weight-loss data.

Research current to 10 July 2026. This is an analysis of the investment case, not personal financial advice.