MannKind

The July FDA Trade, the Real Cash Runway and What the Market May Be Missing

A deep dive into Afrezza, Furoscix, Tyvaso DPI, debt, valuation, upcoming catalysts and the trading opportunity around 26 July.

MannKind MNKD 0.00%↑ is often described as the company behind Afrezza, the inhaled insulin that has spent years trying to break into a market dominated by injectable products.

That description is now badly out of date.

MannKind has become a strange but interesting hybrid: part specialty pharmaceutical company, part drug-manufacturing partner, part royalty business and part clinical-stage biotech. It owns commercial products, receives recurring income from United Therapeutics, carries substantial debt and is developing several new inhaled treatments through its Technosphere platform.

That complexity is probably one reason the market struggles to value it.

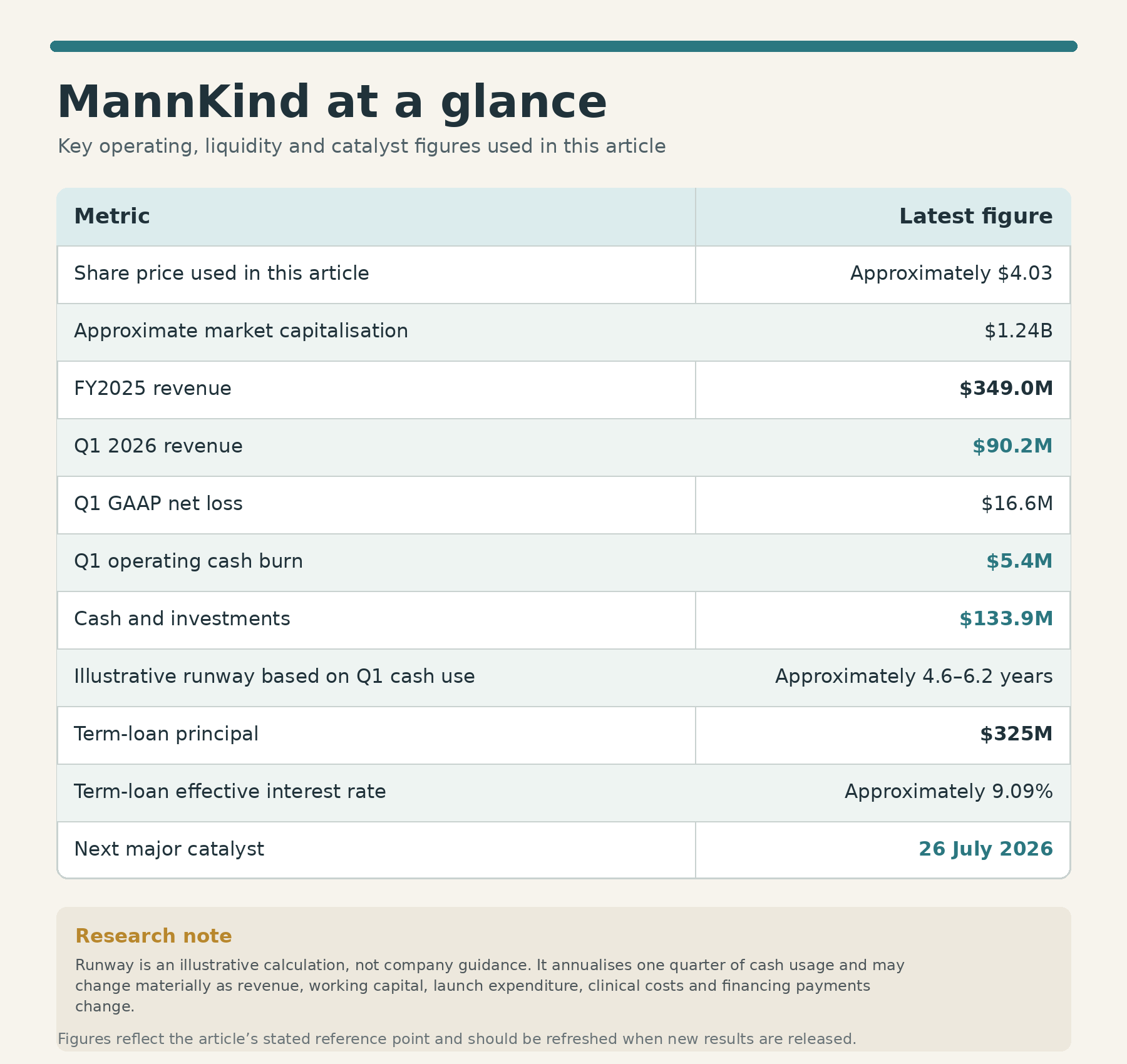

At a share price of approximately $4.03, MannKind is valued at around $1.24 billion. According to the TipRanks screen dated 17 July, analysts have five Buy ratings, one Hold and no Sell ratings, with an average target of $8.15. But the immediate reason traders are watching the stock is much closer: an FDA decision on the new Furoscix ReadyFlow autoinjector, with a target date of 26 July 2026.

MannKind at a glance

What does MannKind actually do?

MannKind now has three principal commercial engines.

The first is Afrezza, an ultra-rapid inhaled mealtime insulin. The second is Furoscix, an at-home treatment for fluid overload associated with heart failure and chronic kidney disease. The third is its partnership with United Therapeutics, under which MannKind manufactures Tyvaso DPI and receives manufacturing income and royalties.

It also owns the smaller V-Go insulin-delivery business and is developing inhaled versions of drugs for pulmonary fibrosis, pulmonary hypertension and fluid overload.

A useful way to think about MannKind is:

Afrezza and Furoscix provide the owned-product opportunity. Tyvaso DPI provides the recurring financial foundation. The pipeline provides the speculative upside.

The quality and risk of these revenue streams are very different.

Where the revenue comes from

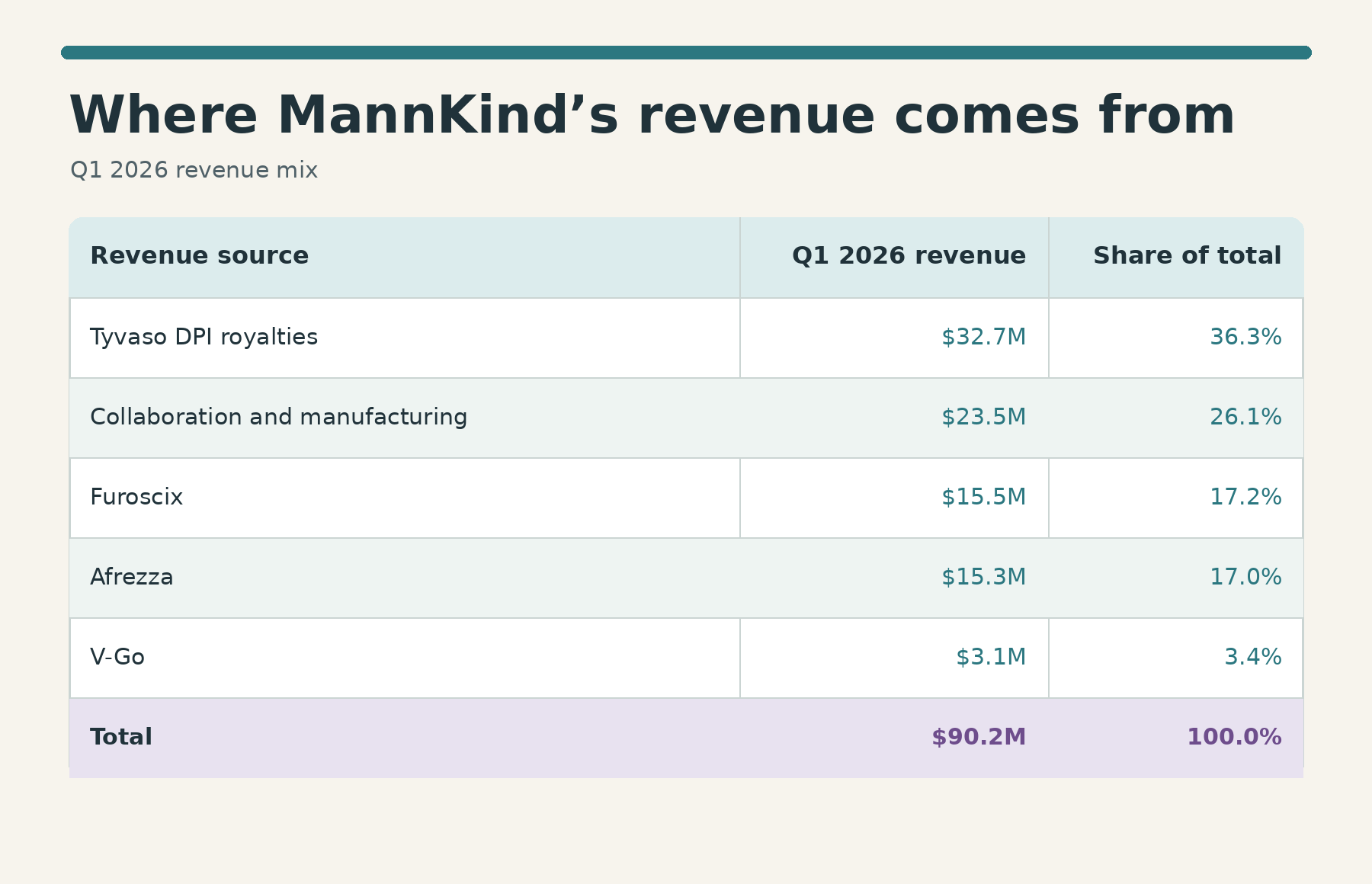

MannKind reported $90.2 million of revenue in Q1 2026, an increase of 15% from the previous year.

Afrezza sales increased only 3%, while Tyvaso DPI royalties increased 9%. Collaboration and manufacturing revenue declined 20%, partly because this revenue can move around depending on United Therapeutics’ ordering and production requirements. Furoscix contributed $15.5 million following MannKind’s acquisition of scPharmaceuticals in October 2025.

Approximately 62% of MannKind’s Q1 revenue came from United Therapeutics when Tyvaso royalties, manufacturing and licence revenue are combined.

That concentration is both MannKind’s greatest strength and one of its largest risks.

United Therapeutics gives MannKind a growing commercial product without MannKind having to fund the entire sales operation. But it also means a large proportion of revenue depends on one partner, one franchise and decisions MannKind does not directly control.

The Tyvaso DPI engine

Tyvaso DPI is an inhaled dry-powder formulation of treprostinil used for pulmonary arterial hypertension and pulmonary hypertension associated with interstitial lung disease.

United Therapeutics handles development and commercialisation, while MannKind manufactures the product and receives royalties.

United Therapeutics reported $330.3 million of Q1 2026 Tyvaso DPI sales, up 9% year over year. MannKind records a contractual royalty equal to 10% of Tyvaso DPI sales, although it previously sold the economic right to one percentage point of that royalty. It therefore retains the economic benefit of approximately 9%.

This is arguably MannKind’s best asset.

Royalty revenue generally requires much less incremental selling expenditure than revenue from a drug MannKind must market itself. As Tyvaso DPI sales grow, a significant proportion of the additional royalty income can potentially flow toward operating profit and cash flow.

However, investors should understand the accounting.

MannKind still reports the full 10% royalty as revenue and records payments connected with the sold royalty interest separately. The associated royalty liability stood at approximately $150.6 million at the end of Q1. This is not a conventional loan requiring immediate repayment, but I would still treat it as a debt-like obligation when making a conservative enterprise-value calculation.

The longer-term IPF opportunity

United Therapeutics has reported positive Phase III results from the TETON programme evaluating nebulised Tyvaso in idiopathic pulmonary fibrosis. In TETON-1, the reported difference in forced vital capacity was 130.1 mL in favour of treatment, with a highly statistically significant result.

United Therapeutics intends to submit an additional application for the nebulised product by the end of summer 2026.

This could eventually benefit MannKind, but there is an important detail: an expanded indication for nebulised Tyvaso would not automatically give Tyvaso DPI the same indication. United Therapeutics has indicated that bridging studies and potentially additional pivotal work may be required for the dry-powder version. It is therefore valuable longer-term optionality, rather than an immediate expansion of MannKind’s royalty base.

Afrezza: an attractive idea that still needs commercial proof

Afrezza is inhaled at the beginning of a meal and acts more rapidly than conventional injected mealtime insulin.

The product’s obvious appeal is convenience. Some patients dislike injections, while Afrezza’s rapid action and relatively short duration may help certain patients manage post-meal glucose without insulin remaining active for as long.

On 29 May 2026, the FDA expanded Afrezza’s approval to include children aged six and older with diabetes. MannKind describes Afrezza as the first and only inhaled insulin approved for paediatric use in the United States. The company estimates that more than 350,000 US children and adolescents are living with diabetes.

That sounds like a major commercial opportunity, but approval does not guarantee rapid adoption.

Afrezza has been available for adults for years, yet Q1 sales were still only $15.3 million. For the paediatric launch to become meaningful, MannKind must persuade doctors, patients, parents, insurers and diabetes educators that the benefits justify changing established treatment routines.

There are also important limitations:

Patients with Type 1 diabetes must still use long-acting basal insulin.

Afrezza is contraindicated in patients with chronic lung diseases such as asthma or COPD because of the risk of acute bronchospasm.

Lung-function testing is required before starting treatment, again after six months and annually thereafter.

It is not recommended for smokers or people who have recently stopped smoking.

Diabetic ketoacidosis occurred more frequently in Afrezza-treated Type 1 diabetes patients in clinical studies than in comparator-treated patients.

None of these limitations makes Afrezza a bad product. They simply help explain why a needle-free insulin has not automatically captured a huge share of the diabetes market.

For investors, the paediatric approval should be judged through actual commercial evidence:

New prescriptions.

Repeat prescriptions and patient retention.

The number of doctors prescribing the product.

Insurance coverage and prior-authorisation requirements.

Discounts and rebates required to generate sales.

Whether revenue growth eventually exceeds the additional sales expenditure.

The next few quarterly reports will be more important than the approval headline itself.

Furoscix: the product behind the July catalyst

Furoscix is a subcutaneous formulation of furosemide, a powerful diuretic used to remove excess fluid.

Patients with worsening heart failure or chronic kidney disease can become overloaded with fluid. Oral diuretics may sometimes become insufficient or inconsistently absorbed, while intravenous furosemide usually requires treatment in a medical facility.

Furoscix attempts to fill the space between those two options by delivering an IV-equivalent dose at home.

The existing Furoscix on-body infusor administers treatment over approximately five hours. MannKind’s new ReadyFlow device is a handheld autoinjector designed to administer the dose in less than ten seconds.

In a bioavailability study, ReadyFlow produced estimated bioavailability of 107.3% relative to intravenous furosemide, with the confidence interval remaining inside the conventional bioequivalence range.

If approved, ReadyFlow could be far easier for patients and clinicians to use than a five-hour wearable device. MannKind has also said that patent protection could potentially extend through 2040.

Furoscix generated $15.5 million in Q1 revenue, while doses dispensed increased 64% year over year. That provides evidence that the franchise already has commercial traction before ReadyFlow enters the market.

ReadyFlow is not entering an empty market. The competitive picture should not be ignored.

The FDA has also approved Lasix ONYU, another subcutaneous furosemide product for adults with chronic heart failure. Like the existing Furoscix device, Lasix ONYU delivers the drug through an on-body system over approximately five hours.

ReadyFlow’s main potential advantage is therefore not that it is the only way to administer furosemide outside a hospital. Its advantage is the possibility of delivering an equivalent dose in seconds rather than hours.

That is a compelling distinction, but commercial success will still depend on:

The final FDA label.

Reimbursement and patient out-of-pocket cost.

Whether cardiologists and nephrologists change their prescribing behaviour.

Whether the device is genuinely easy for older or unwell patients to use.

Manufacturing capacity and product availability.

Evidence that at-home treatment reduces emergency visits or hospital admissions.

Competition from oral, intravenous and other subcutaneous formulations.

One hidden cost of a ReadyFlow approval

MannKind acquired scPharmaceuticals in October 2025, paying $5.35 per share in cash and issuing contingent value rights to former scPharmaceuticals shareholders.

Under those arrangements, ReadyFlow approval by 30 September 2026 can trigger a payment of $0.75 per CVR. A later approval would produce a smaller payment, while additional CVR payments are linked to Furoscix and ReadyFlow sales milestones.

The CVR liability had an estimated fair value of approximately $29 million at the end of March.

This does not undermine the approval thesis, but it is something traders may miss.

A ReadyFlow approval would create commercial value while also creating a cash obligation. The press release may therefore generate excitement, while the subsequent financial statements reveal an associated payment.

The often-quoted $110 million to $120 million Furoscix sales range also needs to be described correctly. It appears in the acquisition’s CVR milestone terms. It should not automatically be presented as formal management revenue guidance.

The pipeline beyond commercial products

MNKD-201

MNKD-201 is MannKind’s inhaled formulation of nintedanib, an established oral treatment for idiopathic pulmonary fibrosis.

Oral nintedanib can be difficult for some patients to tolerate because of systemic adverse effects. MannKind’s research hypothesis is that direct delivery to the lungs may produce useful pulmonary exposure while reducing exposure elsewhere in the body.

That remains a hypothesis—not a proven clinical advantage.

MannKind completed the first cohort of its Phase 1b INFLO-1 study without reported serious adverse events or discontinuations. Topline data are expected during Q3 2026. The company has also started moving the programme toward the Phase II INFLO-2 study.

The Q3 readout should be interpreted primarily as a safety and pharmacokinetic event. Investors should not expect an early study to establish that the product reduces disease progression.

The useful questions will be:

Did inhaled dosing produce adequate drug exposure in the lungs?

Was systemic exposure lower than with oral treatment?

Were gastrointestinal adverse effects reduced?

Did patients tolerate repeated dosing?

Is the selected dose practical for a later-stage study?

MNKD-1501

MNKD-1501 is an inhaled dry-powder version of ralinepag being developed with United Therapeutics for pulmonary hypertension.

MannKind received an upfront payment and can receive additional development milestones, followed by a 10% royalty on a resulting product. The programme adds another potential partner-funded product to the Technosphere platform.

MNKD-701

MNKD-701 is a preclinical inhaled formulation of bumetanide being explored for fluid overload associated with heart failure and chronic kidney disease.

The logic is similar to Furoscix: deliver a potent diuretic without requiring an intravenous visit. But it remains early and should not receive much value in a conservative investment model yet.

One useful research lesson is that pipeline webpages can become stale. MannKind’s previous clofazimine programme was discontinued in Q4 2025, which is why the latest 10-K, 10-Q and earnings release should take priority over an older investor presentation or pipeline graphic.

The fundamentals: growth is real, but so is the spending

MannKind generated $349.0 million of revenue in 2025, up 22%.

The largest components were:

Tyvaso DPI royalties: $128.1 million, up 25%.

Collaboration and service revenue: $106.7 million, up 6%.

Afrezza: $74.6 million, up 16%.

Furoscix: $23.2 million following the October acquisition.

V-Go: $16.4 million, down 10%.

Q1 2026 revenue then grew another 15% to $90.2 million.

However, MannKind is spending heavily to launch and support its expanded portfolio. Q1 research and development expense increased 56% to $17.2 million, while selling, general and administrative expense increased 116% to $54.1 million.

The higher SG&A spending reflects the Furoscix organisation, the scPharmaceuticals acquisition and preparations for the paediatric Afrezza launch.

This is the central fundamental question:

Can revenue grow quickly enough for MannKind’s royalty income and commercial products to absorb the expanded cost base?

A company can report impressive revenue growth and still destroy value if every additional dollar of sales requires even more spending.

For the operating model to work, SG&A growth must eventually slow while Furoscix, Afrezza and royalty revenue continue rising.

Net loss is not the same as cash burn

MannKind reported a Q1 GAAP net loss of $16.6 million, or $0.05 per share. Its non-GAAP adjusted loss was approximately $6.9 million, or $0.02 per share.

However, the company used only $5.4 million of cash in operating activities during the quarter.

Why the difference?

Net income contains non-cash items such as depreciation, amortisation, stock compensation and changes in the value of financial liabilities. Cash flow measures the money that actually entered or left the business during the period.

The reverse can also happen: reported earnings may look acceptable while cash disappears because receivables rise, inventory is built or liabilities are paid.

That is why biotech and pharmaceutical investors should always examine at least three figures together:

Net profit or loss.

Operating cash flow.

Total movement in cash after investing and financing activity.

MannKind’s cash balance fell by much more than its $5.4 million operating burn because it also used approximately $35.5 million to settle the remainder of its convertible notes. That was a financing transaction rather than ordinary operating expenditure.

The real cash runway

MannKind ended Q1 with approximately $133.9 million in cash, cash equivalents and investments.

Using the Q1 operating cash burn of $5.365 million:

$133.9M ÷ $21.46M annualised burn = approximately 6.2 years.

Including Q1 capital expenditure of $1.88 million:

$133.9M ÷ $28.98M annualised cash use = approximately 4.6 years.

That produces the headline runway range of approximately 4.6 to 6.2 years.

But there is another level of analysis.

MannKind’s debt agreement requires it to maintain at least $40 million of liquidity at quarter-end. That means the entire $133.9 million should not be treated as freely spendable.

Subtracting the required $40 million gives approximately $93.9 million of headroom:

Operating-burn basis: approximately 4 years.

Operating burn plus capital expenditure: approximately 3 years.

This covenant-adjusted range is more conservative and, in my view, more useful.

Even that is only a snapshot. It does not include the eventual repayment or refinancing of the $325 million term loan, potential CVR payments, acquisition-related costs or future changes in commercial and clinical spending. Conversely, it also does not assume that revenue and cash generation improve.

MannKind itself states only that its available resources are expected to be sufficient for at least the next 12 months. Companies generally avoid giving the kind of multi-year runway calculation investors often make themselves.

The debt matters

MannKind has $325 million of principal outstanding under its Blackstone term loan.

The loan matures in August 2030 and is largely repayable at maturity rather than gradually amortising. Its effective interest rate was approximately 9.09% at the end of Q1. It is secured against substantially all the company’s assets, including intellectual property.

At a 9.09% effective rate, $325 million represents a rough annual interest burden of around $29.5 million from the term loan alone.

MannKind paid $9.7 million of cash interest across its obligations during Q1. That means the company must generate considerable cash merely to service its capital structure before reducing principal or returning anything to shareholders.

The company may have access to additional financing, including a delayed-draw commitment and potentially larger uncommitted facilities. But access to more debt is not the same as having more equity value. Borrowing can extend liquidity while increasing future interest and refinancing risk.

This is why I would not describe MannKind as financially weak, but I would also not describe the balance sheet as clean.

Near-term dilution does not appear to be the obvious base-case threat. The more important financial risks are debt service, the 2030 maturity, contingent acquisition payments and whether the commercial business reaches sustainable positive cash flow.

Valuation

At approximately $4.03 per share, MannKind’s market capitalisation is around $1.24 billion.

Using $325 million of term-loan debt and $133.9 million of cash and investments produces a conventional enterprise value of approximately:

$1.24B + $325M − $133.9M = $1.43B

Against FY2025 revenue of $349 million:

Market capitalisation to sales: approximately 3.6 times.

Conventional enterprise value to sales: approximately 4.1 times.

Treating the $150.6 million royalty liability as debt-like produces an adjusted enterprise value of approximately $1.58 billion, or roughly 4.5 times FY2025 revenue.

Those multiples are not obviously cheap for a loss-making company, but a simple revenue multiple does not capture the business properly.

A more sensible valuation would separate:

The high-margin Tyvaso DPI royalty stream.

Tyvaso manufacturing and collaboration income.

The Afrezza franchise.

Furoscix and the potential ReadyFlow launch.

The clinical pipeline.

Cash.

Debt, royalty obligations and contingent payments.

The Tyvaso royalty stream deserves a higher multiple than a labour-intensive commercial product because it requires less selling expenditure. Afrezza and Furoscix should be valued on expected future cash flow, not simply headline sales. The pipeline should be heavily probability-adjusted because most early clinical programmes do not reach approval.

What analysts think

According to the TipRanks screen supplied for this research:

Five analysts rate MannKind a Buy.

One rates it a Hold.

None rate it a Sell.

The average target is $8.15.

The high target is $11.

The low target is $4.75.

At a $4.03 share price, the average target implies approximately 102% upside.

Recent published targets include an $11 target from Wells Fargo and a $9 target from Truist, while RBC’s $4.75 target and Hold rating demonstrate that not every analyst sees a major rerating ahead.

Analyst targets can be useful for understanding expectations, but they should not be mistaken for probabilities.

A target usually reflects assumptions about future sales, margins, regulatory outcomes and valuation multiples. When any of those assumptions change, the target changes. An analyst’s $11 scenario also does not protect a trader from a sharp decline following a regulatory disappointment.

The catalyst calendar

24–27 July 2026: ReadyFlow FDA watch window

The official FDA target date is Sunday, 26 July.

Because the date falls on a weekend, traders should be alert from Friday 24 July through Monday 27 July. The FDA can also act ahead of a PDUFA date or, occasionally, communicate later. The date is a target, not a guaranteed announcement appointment.

This is the immediate binary catalyst.

Q3 2026: MNKD-201 Phase 1b results

MannKind expects topline INFLO-1 data for inhaled nintedanib during Q3.

The most important information will be tolerability, pulmonary exposure, systemic exposure and the dose selected for Phase II—not proof of clinical efficacy.

Second half of 2026: paediatric Afrezza launch evidence

Investors should watch prescription growth, payer coverage, the number of new prescribers and whether Afrezza revenue accelerates from the modest 3% growth reported in Q1.

End of summer 2026: United Therapeutics IPF submission

United Therapeutics intends to seek an expanded indication for nebulised Tyvaso following the positive TETON programme. This is an indirect and longer-term MannKind catalyst because the DPI formulation would still require additional development work for the same indication.

Next quarterly report

The next earnings report will provide an important update on Furoscix sales, commercial spending, cash burn and early paediatric Afrezza indicators. I have not found a confirmed reporting date in the primary sources reviewed, so it is better not to present an estimated calendar date as official.

The ReadyFlow trading opportunity

ReadyFlow creates a classic event-driven biotech setup: a defined regulatory date, a product with existing clinical and commercial foundations, and a share price that could respond sharply to the wording of an FDA decision.

But “FDA approval” is not a single uniform outcome.

Bullish outcome

The strongest possible announcement would contain:

Full approval by or before the target date.

A commercially useful label covering the expected heart-failure and kidney-disease populations.

No unexpected safety restrictions.

Immediate or near-immediate product availability.

Clear reimbursement and launch plans.

Confidence that supply can meet demand.

Constructive guidance on switching patients from the existing infusor.

That combination could cause investors to raise Furoscix revenue estimates and assign more value to the scPharmaceuticals acquisition.

Mixed outcome

The FDA could approve ReadyFlow but leave investors underwhelmed because:

The label is narrower than expected.

Launch timing is delayed.

Manufacturing or device supply is limited.

Pricing or reimbursement remains unclear.

Management avoids giving commercial guidance.

Approval was already heavily anticipated by short-term traders.

That could produce a muted reaction or a “sell the news” move despite the positive headline.

Bearish outcome

A Complete Response Letter, material delay or unexpected request for additional data would probably trigger a negative repricing.

The severity would depend on whether the issue is:

Easily correctable manufacturing documentation.

A device or human-factors issue.

A request for additional clinical data.

A broader safety or efficacy concern.

The press release headline will not tell the whole story. Traders should read the explanation of what the FDA requested and how long management expects remediation to take.

Three ways traders can approach it

1. Trade the run-up but exit before the decision

This approach seeks to capture pre-catalyst interest without accepting the full regulatory outcome risk.

The disadvantage is that the stock may not run up, or the FDA could announce its decision earlier than expected.

2. Hold a deliberately small position through the decision

This provides full exposure to a positive gap but also full exposure to a negative one.

Position sizing matters far more than confidence. A sensible binary-event position is one where a severe adverse gap would be painful but not damaging to the overall portfolio.

3. Wait for the result

A trader can wait for the FDA outcome, read the label and launch details, then trade the post-event breakout or subsequent pullback.

This sacrifices some potential upside but removes much of the regulatory uncertainty. It may be the cleaner approach for anyone whose real thesis is commercial adoption rather than the regulatory event itself.

A warning on spread betting

A leveraged spread bet makes binary catalyst risk significantly more dangerous.

FDA news can arrive outside market hours and cause the stock to reopen far above or below the previous price. A normal stop-loss may be executed at the next available price rather than the level selected, meaning the actual loss can be much larger than expected.

For an FDA event, leverage should not be mistaken for conviction.

What to read when the decision arrives

Do not trade solely from the words “FDA approves.”

Read the complete announcement and look for:

The exact indication.

Eligible patient populations.

Dosing and administration requirements.

Safety warnings and monitoring.

Whether the product is available immediately.

Manufacturing and inventory readiness.

Reimbursement and payer plans.

Pricing relative to the current Furoscix device.

Management’s updated commercial expectations.

The resulting CVR payment and effect on cash.

Those details will determine whether approval materially changes future revenue forecasts.

How to research a biotech properly

MannKind is a useful case study because reading only the investor presentation produces an incomplete picture.

Start with the 10-Q and 10-K

The filings show debt terms, customer concentration, contingent obligations, cash flow, acquisition accounting and commitments that may receive little attention in marketing materials.

Separate revenue by quality

A dollar of royalty revenue is not economically identical to a dollar of product revenue.

Ask who pays the selling costs, who controls the product, whether the revenue is recurring and how much direct expenditure is required to generate the next dollar.

Reconcile profit with cash

Look at net income, operating cash flow, capital expenditure and financing activity separately. MannKind’s Q1 cash decline would look alarming without recognising that $35.5 million went toward settling convertible notes.

Calculate more than one runway

A proper runway analysis should include:

Cash divided by operating burn.

Cash divided by operating burn plus capital expenditure.

Available cash above debt covenants.

Debt maturities and likely refinancing needs.

Contingent payments.

Whether revenue is growing quickly enough to reduce future burn.

Read the FDA label

A press release highlights the opportunity. The FDA label reveals who can actually use the product, contraindications, required monitoring and warnings that may limit adoption.

Research the partner

Because United Therapeutics generates approximately 62% of MannKind’s revenue, its filings and earnings calls are essential MannKind research.

A MannKind investor who never reads United Therapeutics’ results is missing a large part of the thesis.

Check ClinicalTrials.gov

Look at trial design, enrolment, endpoints, comparison groups, estimated completion dates and whether the study status has changed. Company timelines are useful, but the trial registry provides a second source.

Read acquisition agreements

The ReadyFlow CVR shows why acquisition terms matter. A successful catalyst can create an asset while simultaneously triggering a cash payment.

Use analyst targets last

Build the thesis first. Then compare it with analysts to identify where your assumptions differ.

The bull case

The strongest MannKind argument is that the company has finally built enough scale and diversification to move beyond the old Afrezza-only story.

Tyvaso DPI provides growing royalty and manufacturing income. Furoscix already has commercial momentum, with ReadyFlow potentially making the franchise much easier to use. Afrezza now has access to a paediatric population. MNKD-201 and the broader inhaled pipeline offer additional upside.

Cash burn was modest in Q1 relative to the available cash balance, and immediate equity dilution does not appear necessary under the current trajectory.

If revenue keeps growing while SG&A stabilises, MannKind could move from a loss-making hybrid into a genuinely cash-generative specialty pharmaceutical company.

The bear case

The balance sheet is heavily leveraged, with $325 million of term debt, expensive interest and a 2030 maturity that will eventually require repayment or refinancing.

United Therapeutics accounts for approximately 62% of revenue, leaving MannKind exposed to one partner and one product franchise.

Afrezza’s commercial history shows that an attractive medical concept does not always produce rapid adoption. Furoscix and ReadyFlow must compete with established oral and IV furosemide as well as another FDA-approved subcutaneous device.

SG&A has more than doubled, meaning strong product growth is required simply to absorb the enlarged commercial organisation.

ReadyFlow approval may already be partly priced in, while a regulatory setback could produce an immediate negative gap.

My conclusion

MannKind is much more interesting than the old “inhaled insulin company” description suggests.

The Tyvaso DPI partnership has created a valuable recurring revenue stream. Furoscix gives the company a credible second owned franchise. ReadyFlow could make that franchise considerably more useful, while paediatric Afrezza and MNKD-201 add further optionality.

But this is not a simple undervalued biotech with a huge cash pile.

MannKind carries substantial debt, unusual royalty obligations, contingent acquisition payments and a rapidly expanded cost base. Its reported runway looks comfortable at approximately 4.6 to 6.2 years, but the covenant-adjusted cushion is closer to 3.2 to 4.4 years, and the $325 million loan maturity in 2030 cannot be ignored.

For traders, the 26 July ReadyFlow decision is the immediate opportunity.

For longer-term investors, approval is only the beginning. The real proof will come from prescription growth, reimbursement, commercial margins and whether MannKind can convert its enlarged product portfolio into sustainable positive cash flow.

At approximately $4.03, the stock offers meaningful upside if the bull case develops—but it also carries enough regulatory, commercial and balance-sheet risk that position sizing matters far more than any analyst price target.

This article is for research and educational purposes only. It is not personal financial advice. Biopharmaceutical stocks can move sharply following regulatory, clinical and commercial news, and leveraged positions can lose more than expected.